Knowing your car loan eligibility is essential before applying for a vehicle loan. Your eligibility not only influences whether your loan application gets approved but also affects the terms you receive, such as the interest rate, loan amount, and repayment duration. Being aware of these criteria upfront helps you avoid unnecessary delays and increases your chances of a smooth loan approval process.

Lenders evaluate several factors to determine your eligibility, including your age, income level, employment status, credit score, and current financial liabilities. Meeting these requirements improves your likelihood of approval and can lead to more favourable loan terms, such as lower interest rates and higher borrowing limits.

This article will guide you through the key eligibility factors for car loans. By understanding what lenders expect, you can better prepare your application, enhance your financial standing, and approach lenders confidently. Whether you’re employed, self-employed, or a business owner, this knowledge will empower you to choose the best car loan option tailored to your needs.

2. What is Car Loan Eligibility?

Car loan eligibility refers to the specific criteria that a borrower must meet to qualify for a car loan. These guidelines help lenders evaluate whether an applicant has the financial capacity and creditworthiness to repay the loan amount without defaulting. Key factors typically considered include your age, monthly income, job stability, credit score, current debts, and residential history.

Lenders assess eligibility to minimize lending risk and ensure the borrower can handle the repayment comfortably. This evaluation process helps financial institutions decide not only whether to approve your application but also the loan amount, interest rate, and repayment terms they are willing to offer.

Although the exact criteria may vary from one lender to another, the core objective remains the same: to confirm that the borrower is financially stable and reliable. By understanding these eligibility requirements in advance, you can improve your financial profile and gather the necessary documents to strengthen your application.

Being aware of your loan eligibility before applying can help you avoid unnecessary rejections, streamline the approval process, and secure better loan terms tailored to your financial situation.

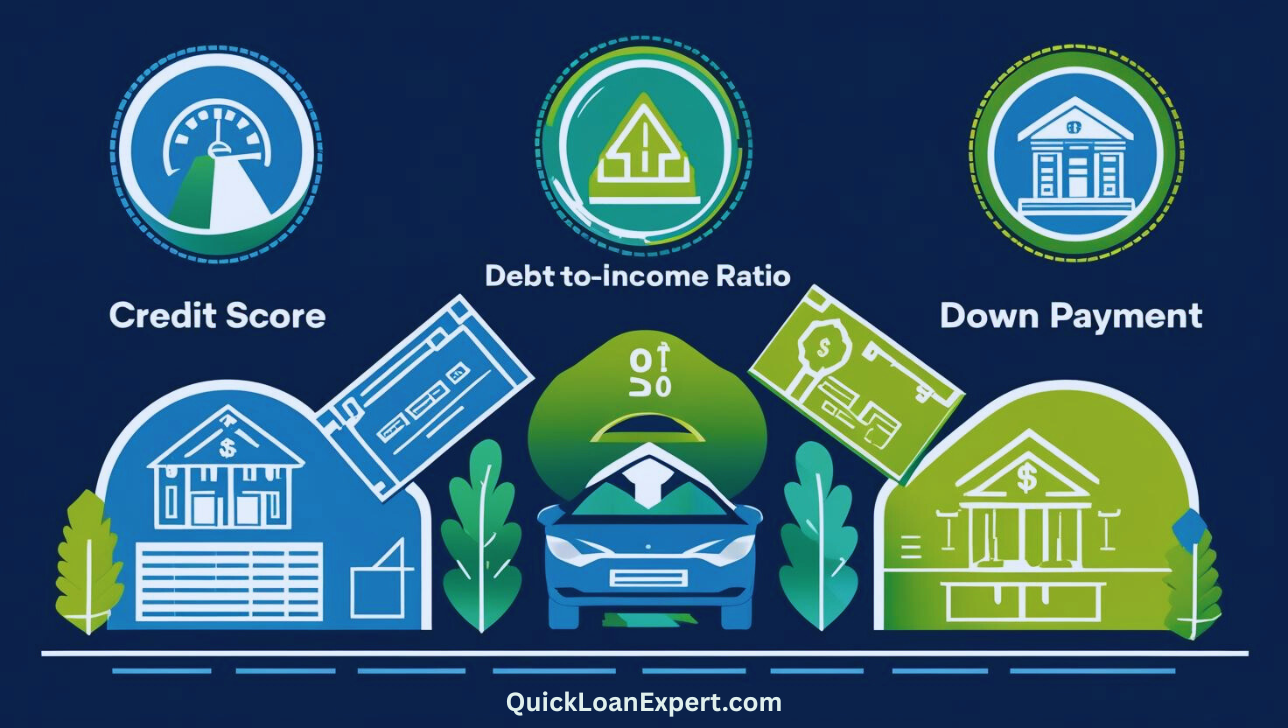

3. Key Eligibility Factors for Car Loans

Before approving a car loan, lenders carefully assess several eligibility parameters to determine if you’re a suitable candidate. Understanding these factors can help you prepare better and improve your chances of loan approval.

Age Requirements: Most financial institutions require borrowers to be between 21 and 65 years old, ensuring they are legally and financially capable of repaying the loan within the tenure.

Income Criteria: A stable and sufficient income is essential. Salaried professionals usually need to earn a minimum of ₹15,000 to ₹25,000 per month, while self-employed individuals must show steady income through bank records or filed tax returns.

Employment Status: Consistent employment or a well-established business history of at least 1–2 years boosts your loan eligibility, as it reflects financial stability.

Credit Score: A credit score of 700 or higher is ideal. Good credit history increases your approval chances and may qualify you for lower interest rates.

Existing Debt Obligations: Your debt-to-income ratio is analysed to ensure you can handle new EMIs without straining your finances.

Residential Stability: Long-term residence at your current address, along with valid proof, enhances credibility and reduces perceived lending risk.

4. Required Documentation for Car Loan Approval

To get your car loan application approved quickly and efficiently, it’s essential to provide accurate and complete documentation. These documents help the lender verify your identity, income, and the purpose of the loan, allowing them to assess your eligibility and creditworthiness.

Identity Proof: You’ll need to submit valid photo identification such as an Aadhaar card, PAN card, passport, voter ID, or driving license.

Income Proof:

Salaried employees are required to provide recent salary slips (typically last 3–6 months) along with bank statements.

Self-employed individuals must submit Income Tax Returns (ITRs), profit and loss statements, and bank statements to demonstrate steady income.

C. Address Proof: Documents like utility bills, Aadhaar card, rental agreement, or passport are accepted as proof of residence.

D. Proof of Employment or Business:

Salaried professionals can submit an employment letter or company ID.

Self-employed applicants should provide business registration certificates, GST filings, or trade licenses.

E. Additional Documents: You may also need to provide car details, such as the dealer’s quotation or invoice, and proof of any down payment made.

Submitting complete documents upfront helps streamline the approval process and enhances your chances of loan approval.

5. Eligibility Criteria Variations for Different Borrower Types

Car loan eligibility criteria differ based on the applicant’s profession and residential status. Recognizing these distinctions can help you better understand what lenders expect and improve your chances of approval.

Salaried Individuals: For salaried professionals, lenders generally require steady employment with at least 1–2 years of work experience. A minimum monthly income—often between ₹15,000 and ₹25,000—is essential, along with a healthy credit score. Working with a reputed employer can also enhance your loan eligibility.

Self-Employed Professionals: Professionals such as doctors, architects, and consultants must provide proof of consistent earnings through Income Tax Returns and bank statements. Most banks expect at least 2–3 years of stable practice, along with valid business documentation like professional licenses or registrations.

Business Owners: Entrepreneurs need to demonstrate a minimum of two years of stable business income. Required paperwork includes audited financials, ITRs, business registration certificates, and GST filings to establish income reliability.

NRIs (Non-Resident Indians): NRIs can also apply for car loans in India, though requirements are more stringent. Most lenders require proof of foreign employment, valid visa documents, an NRI account in India, and a resident Indian co-applicant.

Understanding these tailored criteria helps you apply more confidently and efficiently.

6. How to Improve Your Car Loan Eligibility

Enhancing your car loan eligibility can significantly improve your chances of loan approval and help you secure better terms. Here are key strategies to strengthen your loan profile:

A. Improve Your Credit Score: Lenders rely heavily on your credit score to assess risk. Pay all existing EMIs and credit card bills on time, avoid late payments, and keep your credit utilization below 30% to boost your score over time.

B. Lower Existing Financial Obligations: Reducing your current debts improves your debt-to-income ratio, making you more creditworthy. Clear off smaller loans and manage outstanding credit card dues before applying for a car loan.

C. Ensure Complete and Correct Documentation: Providing accurate and up-to-date documents—including ID proof, income proof, address verification, and vehicle details—can speed up the loan process and avoid unnecessary delays or rejections.

D. Maintain Stable Income and Job History: A consistent source of income and long-term employment or business track record reassures lenders of your repayment capability. Ideally, have at least 1–2 years of steady employment or business income.

Taking these proactive steps can greatly enhance your loan application and position you for better loan offers.

7. Common Reasons for Car Loan Rejection

Having your car loan application declined can be disappointing, but knowing the typical causes can help you improve your chances in the future.

Poor Credit History: A low credit score or records of missed payments and defaults are major red flags for lenders. Such a credit profile indicates higher risk, often resulting in loan denial or higher interest rates.

Insufficient Income or Unstable Employment: Lenders need assurance of steady and adequate income to approve a loan. If your income is below the lender’s minimum requirement or your employment history is inconsistent, your application may be rejected.

Incomplete or Incorrect Documentation: Failing to provide all required documents or submitting inaccurate paperwork can delay processing or lead to outright refusal. Proper ID, proof of income, address verification, and car details are critical for approval.

High Existing Debt Burden: A high debt-to-income ratio indicates you may struggle to repay new loans. Existing loans, credit card balances, or EMIs that consume a large part of your income reduce your loan eligibility.

By addressing these common issues beforehand, you can strengthen your application and increase your chances of car loan approval.

8. How Lenders Calculate Loan Eligibility Amount

Knowing how lenders determine your car loan eligibility amount can help you plan your application effectively. Several financial aspects are analysed to decide the maximum loan you qualify for.

Income, Expenses, and Credit Score: Lenders evaluate your monthly income in relation to your expenses to assess your repayment ability. A steady income and a strong credit score boost your chances of securing a higher loan amount. On the other hand, high expenses or a poor credit score can reduce the loan limit.

Debt-to-Income Ratio (DTI): The debt-to-income ratio is a key factor in eligibility assessment. It compares your total monthly debt payments—including existing loans and credit cards—to your income. A lower DTI, generally under 40%, indicates you have sufficient capacity to take on additional loan repayments.

Loan-to-Value Ratio (LTV): LTV is the percentage of the car’s price the lender is willing to finance. For example, with an LTV of 80% on a ₹10 lakh car, you could get a loan up to ₹8 lakhs, while you’d need to arrange the remaining ₹2 lakhs as a down payment.

Understanding these calculations can help you estimate your eligible loan amount and improve your chances of approval.

9. Conclusion

Knowing the essential eligibility criteria for a car loan can make all the difference in securing approval and getting favourable loan terms. Key factors such as your age, income level, job stability, credit score, and existing debts influence how much you can borrow and the interest rate you receive. Submitting complete and accurate documents also helps streamline the approval process.

Before you apply, it’s important to evaluate your personal financial situation thoroughly. Understanding your income, outstanding debts, and credit standing allows you to select a loan amount and repayment plan that suits your budget comfortably. Addressing any eligibility gaps ahead of time will improve your chances of loan approval.

Don’t let confusion or doubt delay your car purchase. Check your car loan eligibility today with our simple online tools or consult our loan experts for tailored advice and support. We’re dedicated to helping you find the best financing option that fits your needs and helps you drive home your dream car without hassle.

Take the first step towards easy car financing now!

Frequently Asked Questions About Car Loan Eligibility Criteria

1. What are the key eligibility requirements for a car loan?

Lenders generally look for minimum age, income levels, stable employment, and a good credit score when approving car loans.

2. What is the minimum age to qualify for a car loan?

Most lenders require borrowers to be at least 21 years old, with a maximum age limit usually set between 60 and 65 years at the end of the loan tenure.

3. How does income impact my car loan eligibility?

Your monthly income is a major factor in assessing your repayment capacity. Higher and steady income increases your chances of approval and better interest rates.

4. Are self-employed individuals eligible for car loans?

Yes, but self-employed applicants need to submit additional proofs like income tax returns, business registration certificates, and bank statements to demonstrate steady income.

5. How significant is my credit score in getting a car loan?

A strong credit score, typically above 700, greatly improves loan approval chances and helps secure lower interest rates.

6. Does having existing loans affect my eligibility?

Yes, lenders evaluate your debt-to-income ratio. High existing debt can limit the loan amount you’re eligible for.

7. What documents are needed to verify eligibility?

You’ll typically need identity and address proof, income statements, employment verification, and sometimes bank statements.

8. Can NRIs apply for car loans in India?

Yes, many lenders offer car loans to NRIs, though additional documents like overseas income proof and valid visa are required.

9. How much employment history do lenders expect?

Most lenders prefer applicants to have at least 1 to 2 years of consistent employment or business operation.

10. How can I improve my chances of car loan approval?

Maintain a good credit score, reduce outstanding debts, keep a stable income source, and provide complete and accurate documentation.